Bear Call Spread

Basics of stock market

• Induction

• Bull call spread

• Bull put spread

• Call ration Back spread

• Bear call ladder

• Synthetic long & Arbitrage

• Bear put spread

• Bear call spread

• put ration back spread

• Long straddle

• Short straddle

• Max pain & PCR ratio

• Iron condor

8.1 – Choosing Calls over Puts

The Bear Call Spread is a two-legged option strategy that is used when the market outlook is “moderately bearish,” similar to the Bear Put Spread. In terms of payoff structure, the Bear Call Spread is comparable to the Bear Put Spread, but there are some differences in terms of strategy execution and strike choice. The Bear Call spread entails using call options rather than put options to create a spread (as is the case in bear put spread).

At this point, you might be asking yourself why one would choose a bear call spread over a bear put spread when the payouts from both spreads are comparable.

Strategy Notes

To be honest, a lot will depend on how appealing the premiums are. The Bear Call spread is executed for a credit, as opposed to the Bear Put spread, which is executed for a debit. Therefore, if the market is at a point where –

- The markets have rallied considerably (therefore CALL premiums have swelled)

- The volatility is favorable

- Ample time to expiry

Invoking a Bear Call Spread for a net credit instead of a Bear Put Spread for a net debit makes sense if you have a moderately bearish outlook for the future. Personally, I favour strategies that offer net credit over those that offer net debit.

8.2 – Strategy Notes 2.0

The Bear Call Spread is a two leg spread strategy traditionally involving ITM and OTM Call options. However you can create the spread using other strikes as well. Do remember, the higher the difference between the two selected strikes (spread), larger is the profit potential.The Bear Call Spread is a two leg spread strategy traditionally involving ITM and OTM Call options. However you can create the spread using other strikes as well. Do remember, the higher the difference between the two selected strikes (spread), larger is the profit potential.

Using the bear call spread requires:

- Buy 1 OTM Call option (leg 1)

- Sell 1 ITM Call option (leg 2)

Ensure –

- All strikes belong to the same underlying

- Belong to the same expiry series

- Each leg involves the same number of options

Let us take up example to understand this better –

Date – February 2016

Outlook – Moderately bearish

Nifty Spot – 7222

Bear Call Spread, trade set up –

Pay Rs. 38 as a premium to purchase a 7400 CE; keep in mind that this is an OTM option. This is a debit transaction because money is being taken out of my account.

Selling the 7100 CE will earn you Rs. 136 as premium; keep in mind that this is an ITM option. This is a credit transaction because I receive money.

Since the net cash flow is positive (136 – 38 = +98), my account has a net credit as a result of the difference between the debit and credit.

A bear call spread is also known as a “credit spread” because, generally speaking, there is always a “net credit” in them. The market may move in any direction and expire at any level after we place the trade. In order to understand what would happen to the bear put spread at various levels of expiry, let’s consider a few scenarios.

The market expires in scenario 1 at 7,500. (above the long Call)

Given that we paid a premium of Rs. 38 for 7400 CE, which has an intrinsic value of 100, we would be in the black by the amount of 100 minus 38, or 62.

The intrinsic value of 7100 CE would be 400, and since we sold this option at Ra.136, we would have suffered a loss of 400 – 136 = -264.

A net loss of -264 + 62 = -202 would result.

The market expires at 7400 in scenario two (at the long call)

The 7100 CE would have intrinsic value at 7400 and would therefore expire in the money. The value of the 7400 CE would expire.

- 7400 CE would expire worthless, hence the entire premium of Rs.38 would be written of as a loss.

- 7100 CE would have an intrinsic value of 300, since we have sold this option at Ra.136, we would incur a loss of 300 – 136 = -164

- Net loss would be -164 -38 = – 202

Be aware that the loss at 7400 and 7500 are comparable, indicating that the loss is capped at 202 above that point.

The market expires in scenario 3 at 7198. (breakeven)

7198 is regarded as a breakeven point because at this price, the trade is neither profitable nor unprofitable. Let’s look at how these numbers turn out.

The 7100CE would terminate at 7198 with an intrinsic value of 98. Since we sold the option for Rs. 136, we get to keep a portion of the premium, or 136 – 98 = +38. 7400 CE would expire worthless, so we would forfeit the premium, or 38.

This demonstrates unequivocally that at 7198, the strategy is neutrally profitable.

Situation 4: The market closes at 7100 (at the short call)

Both of the Call options would expire worthless at 7100, making them both worthless and out of the money.

7100 will also have no intrinsic value, so the entire premium received, or Rs. 136, will be retained back. 7400 will have no value, so the premium paid will be a complete loss, or Rs. 38.

136 – 38 = 98 would be the net profit.

It is obvious that the strategy generates a profit as and when the market declines.

8.3 – Strategy Generalization

We can generalise the strategy’s key trigger points based on the aforementioned payoff:

Spread: 7400 minus 7100, or the difference between the strikes, is 300.

Net Credit is calculated as Premiums Paid – Premiums Received (136 – 38 = 98).

Lower strike plus Net Credit 7100 + 98 = 7198 to reach breakeven.

Net Credit = Maximum Profit

Maximum Loss: Spread – Net Credit (300 – 98) = 202

At this point, we can sum the Deltas to determine the overall position delta and determine how sensitive the strategy is to directional movement.

I obtained the following Delta values from the BS calculator:

7400 CE has a delta of +0.32 and is an OTM option.

Since we are short 7100 CE, the delta is -(+0.89) = -0.89 since 7100 CE is an ITM option with a delta of +0.89.

Position delta overall is = +0.32 + (-0.89) = -0.57.

The strategy’s negative delta means that it makes money when the underlying value decreases and loses money when the value increases.

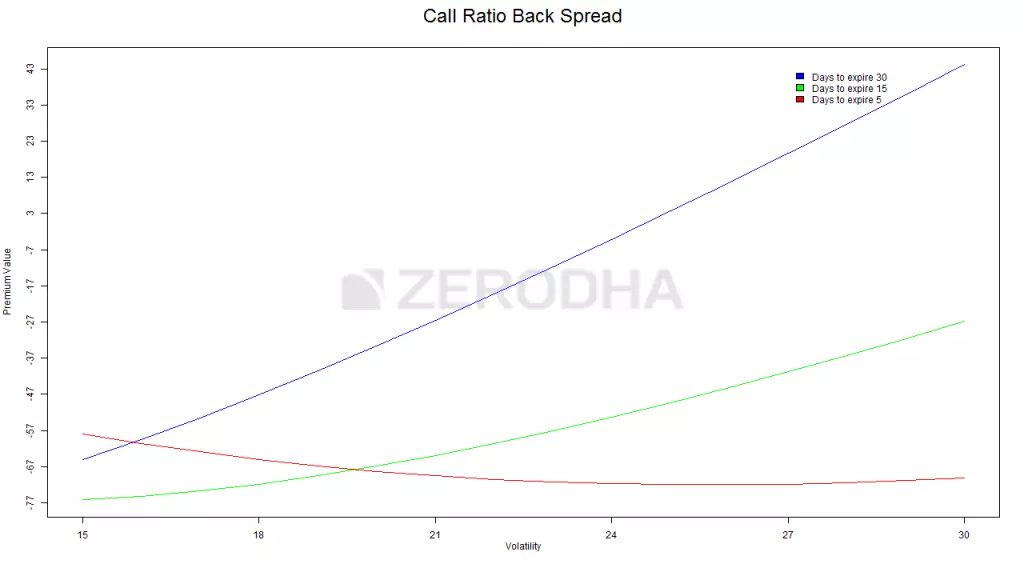

8.4 – Strike Selection and impact of Volatility

The graph above explains how the premium varies with respect to variation in volatility and time.

- The blue line suggests that the cost of the strategy does not vary much with the increase in volatility when there is ample time to expiry (30 days)

- The green line suggests that the cost of the strategy varies moderately with the increase in volatility when there is about 15 days to expiry

- The red line suggests that the cost of the strategy varies significantly with the increase in volatility when there is about 5 days to expiry

It is obvious from these graphs that when there is enough time before expiration, one shouldn’t be overly concerned about changes in volatility. However, between the series’ midpoint and its expiration, one should have an opinion on volatility. The bear call spread is best avoided if you anticipate a decrease in volatility; otherwise, it is advised to use it only when an increase is anticipated.