What will you study in this Mutual funds?

Course Details

__________________________________________

Language: English & Hindi I Time Duration: 1 Day I Fees: 900

In mutual funds, Everyone wants to invest, but only a small percentage of people actually do. What is the reason for this? It’s because many people regard investing as a mystery and a difficult endeavour while, in fact, it is the polar opposite.

Additionally, the Mutual Funds course debunks the myths surrounding mutual fund investment (with a specific focus on the Indian mutual fund industry),

I start with the fundamentals of investing and walk you through the baby steps of learning what a mutual fund is, what a SIP is, and so on, before moving on to more complex topics like STP, SWP, and liquid funds.

_________________________________________________________________

Meanwhile, Let us give you some theoretical knowledge

In India, the mutual fund business has grown to be very important. It’s a key aspect of the capital market, offering a diverse portfolio and competent fund management to a huge number of investors, especially small ones. The demand for mutual fund operations has grown dramatically as the ability to deploy capital through markets has improved.

This session is designed to provide a broad and in-depth understanding of mutual funds.

What is a Mutual Fund?

Whereas, Mutual funds can appear difficult or daunting to many people. We’ll try to break things down for you at the most fundamental level. A Mutual Fund is essentially a collection of money contributed by a big number of people (or investors). A professional fund manager is in charge of this fund.

It’s a trust that gathers funds from a group of participants with a shared investing goal. The money is then invested in stocks, bonds, money market instruments, and/or other securities. Units, which reflect a share of the fund’s holdings, are owned by each investor. By establishing a scheme’s “Net Asset Value,” the income/gains earned from this collective investment are dispersed proportionately among the investors after deducting certain fees.

When is the right time to start investing?

The best time to invest was yesterday. The next best time is now. ever heard this one before? it means that the right time to begin investing is ‘as soon as you can.’

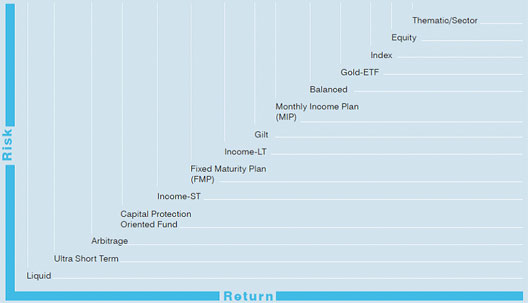

Risk/Return trade-off by mutual fund category on the chart below

Understanding Mutual Funds

Understanding, Mutual funds aggregate money from investors and use it to purchase other securities, most commonly stocks and bonds. The mutual fund company’s worth is determined by the performance of the securities it purchases. As a result, when you purchase a mutual fund unit or share, you are purchasing the portfolio’s performance or, more specifically, a portion of the portfolio’s value. Investing in a mutual fund is not the same as investing in individual stocks. Unlike stock, mutual fund shares do not provide voting rights to their owners. Instead of a single holding, a mutual fund share represents investments in a variety of stocks (or other securities).

A mutual fund is both a financial investment and a legal entity. This dual nature may appear odd, but it is no different than how an AAPL share represents Apple Inc. When an investor buys Apple stock, he is purchasing a portion of the company’s stock and assets. A mutual fund investor, on the other hand, is purchasing a portion of the mutual fund firm and its assets. The distinction is that Apple makes revolutionary devices and tablets, whereas a mutual fund company makes investments.

Types of mutual funds

Types of Mutual funds are classified into a variety of categories based on the securities they have chosen for their portfolios and the type of returns they seek. For practically every sort of investor or investment strategy, there is a fund. Money market funds, sector funds, alternative funds, smart-beta funds, target-date funds, and even funds of funds, or mutual funds that buy shares in other mutual funds, are all typical forms of mutual funds.

The most common type is equities or stock funds. This type of fund invests mostly in equities, as the name suggests. There are several subcategories within this group. Small-, mid-, and large-cap equity funds are named after the size of the firms they invest in. Others are labelled according to their investment strategy: aggressive growth, income-oriented, value, and so on. Equity funds are also classified according to whether they invest in domestic (U.S.) or international (foreign) companies. Because there are so many various kinds of equities, there are so many distinct types of equity funds.

The objective is to categorise funds based on the size of the companies they invest in (market capitalization) as well as the growth possibilities of the stocks they hold. The term “value fund” refers to an investment strategy that seeks out high-quality, low-growth companies that are undervalued by the market. Low price-to-earnings (P/E) ratios, low price-to-book (P/B) ratios, and high dividend yields describe these companies. Spectrums, on the other hand, are growth funds that invest in companies that have had (or are expected to have) substantial earnings, sales, and cash flow growth. These businesses usually have a high P/E ratio and don’t pay dividends.

The fixed-income category is another significant group. A fixed-income mutual fund invests in fixed-income securities such as government bonds, corporate bonds, and other debt instruments that provide a fixed rate of return. The premise is that the fund portfolio earns interest and then distributes it to the shareholders.

These funds, sometimes known as bond funds, are frequently actively managed and seek to buy undervalued bonds in order to sell them for a profit. Bond funds are more likely to produce larger returns than certificates of deposit and money market investments, but they are not risk-free. Bond funds can vary considerably depending on where they invest due to the many different types of bonds available.

Another type of investment that has gained a lot of traction in recent years is known as “index funds.” Their investment strategy is predicated on the premise that regularly beating the market is difficult and expensive. As a result, the index fund manager purchases companies that correlate to a significant market index.This technique necessitates less research from analysts and consultants, resulting in fewer expenses devouring profits before they are passed on to shareholders. Often, these funds are created with cost-conscious investors in mind.

Stocks, bonds, money market instruments, and alternative assets are all part of a balanced fund’s portfolio. The goal is to minimise exposure risk across asset types. An asset allocation fund is another name for this type of vehicle. There are two types of mutual funds created to meet the needs of investors.

Some funds are defined by a fixed allocation approach, allowing investors to have predictable exposure to different asset classes. Other funds use a dynamic allocation percentages technique to accomplish diverse investor goals. This could involve reacting to market conditions, business cycle shifts, or the investor’s own life stages.

The money market consists largely of government Treasury notes, which are safe (risk-free) short-term debt instruments. This is a secure location to keep your funds. You won’t get a lot of money back, but you won’t have to worry about losing your money. A typical return is slightly higher than that of a conventional checking or savings account and slightly lower than that of a certificate of deposit (CD). While money market funds invest in ultra-safe assets, some money market funds suffered losses during the 2008 financial crisis when their share prices fell below that threshold and broke the buck.

The goal of income funds is to offer current income on a consistent basis. These funds primarily invest in government and high-quality corporate debt, keeping bonds until they mature to generate interest payments. While fund holdings may increase in value, the primary goal of these funds is to offer investors with consistent cash flow. As a result, the target market for these funds is conservative investors and retirees. Tax-aware investors may want to avoid these funds because they offer consistent income.

The exchange traded fund is a variation on the mutual fund (ETF). These increasingly popular investment vehicles combine investments and apply mutual fund strategies, but they are organised as investment trusts that are traded on stock markets and offer the extra benefits of stock features. ETFs, for example, can be purchased and sold at any time during the trading day. ETFs can also be bought on leverage or sold short. ETFs also have cheaper fees than their mutual fund counterparts. Active options markets, where investors can hedge or leverage their positions, benefit many ETFs. ETFs and mutual funds both have tax advantages. ETFs are typically less expensive and more liquid than mutual funds.

A mutual fund’s expenses are divided into two categories: annual running fees and shareholder fees. Annual fund operating costs are a percentage of the assets under management that typically range from 1% to 3%. The expense ratio is the sum of all annual operating fees. The expense ratio of a fund is the sum of the advisory or management charge plus the fund’s administrative costs.

Investors pay shareholder fees directly when purchasing or selling mutual funds in the form of sales charges, commissions, and redemption fees. The “load” of a mutual fund refers to the sales charges or commissions. Fees are levied when shares are purchased in a mutual fund with a front-end load.

Advantages of Mutual Funds

For decades, mutual funds have been the vehicle of choice for regular investors for a variety of reasons. Mutual funds receive the vast bulk of money in employer-sponsored retirement plans. Over time, multiple mergers have resulted in mutual funds.

A mutual fund is something you should seriously consider adding to your investing portfolio, whether you are a seasoned or first-time investor. However, you should be aware of both the benefits and potential drawbacks of this investment.

The benefits and drawbacks of mutual funds are listed below to help you make an informed selection.

One of the benefits of investing in mutual funds is diversification, or the mixing of investments and assets within a portfolio to reduce risk. Diversification, according to experts, is a good method to boost a portfolio’s profits while lowering its risk. Diversification can be achieved by purchasing individual firm equities and offsetting them with industrial sector stocks, for example. A fully diversified portfolio, on the other hand, includes securities of various capitalizations and industries, as well as bonds of various maturities and issuers. Buying a mutual fund is a more cost-effective and time-efficient way to diversify than buying individual assets. Hundreds of different equities in a variety of industries are often held by large mutual funds. It would be impossible for an investor to establish such a portfolio with such a modest sum of money.

Mutual funds can be bought and sold with relative ease on the major stock exchanges, making them extremely liquid investments. Furthermore, when it comes to particular asset classes, such as foreign equities or exotic commodities, mutual funds are frequently the most accessible—and in some cases, the only—way for individual investors to engage.

Economies of scale are also provided by mutual funds. Purchasing one saves the investor the time and expense of paying many commissions to build a diversified portfolio. Buying just one security at a time results in high transaction fees, which eat up a significant portion of the investment. Because mutual funds come in smaller denominations, investors can benefit from dollar cost averaging.

The fact that you don’t have to pick stocks or manage assets is a major benefit of mutual funds. Instead, a professional investment manager handles everything with meticulous study and expert trading. Investors buy funds because they don’t have the time or skill to manage their own portfolios, or because they don’t have access to the same information as a professional fund. A mutual fund is a low-cost solution for a small investor to hire a full-time manager to handle and monitor his or her investments. The majority of private, non-institutional money managers exclusively work with high-net-worth customers who have at least six figures to invest. However, as previously stated, mutual funds have far lower investment minimums.

Investors have the option to investigate and choose from a wide range of managers with different management styles and objectives. A fund manager, for example, might specialise in value investing, growth investment, established markets, emerging markets, income investing, or macroeconomic investing, among other things. A single manager may be in charge of funds that apply a variety of strategies. Through specialist mutual funds, investors can acquire exposure to not only equities and bonds, but also commodities, foreign assets, and real estate. Some mutual funds are even designed to profit from a market decline (known as bear funds). Mutual funds provide access to foreign and domestic investment opportunities that would otherwise be unavailable to regular investors.

Mutual funds are governed by industry regulations that assure investor accountability and fairness.

Pros

Liquidity

Diversification

Minimal investment requirements

Professional management

Variety of offerings

Cons

High fees, commissions, and other expenses

Large cash presence in portfolios

No FDIC coverage

Difficulty in comparing funds

Lack of transparency in holdings

Disadvantages of Mutual Funds

Mutual funds appeal to younger, rookie, and other individual investors who don’t want to actively manage their money because of their liquidity, diversity, and expert management. However, no asset is without flaws, and mutual funds are no exception.

There is always the potential that the value of your mutual fund will depreciate, just like many other non-guaranteed investments. Equity mutual funds, like the stocks that make up the fund, are subject to price changes.

However, Mutual funds aggregate money from thousands of investors, allowing them to invest and withdraw money on a daily basis.

To keep a substantial component of their portfolios in cash to facilitate withdrawals, funds must normally hold a large number of their portfolios in cash. Having a lot of cash is great for liquidity, but the money that is just lying around and not working for you isn’t so great.

To satisfy daily share redemptions, mutual funds must hold a considerable portion of their assets in cash.

Funds must often keep a bigger amount of their portfolio in cash than a normal investor to preserve liquidity and the ability to handle withdrawals.

Professional management is provided by mutual funds, but it comes at a cost—those expense ratios discussed earlier. These costs lower the overall payout of the fund and are charged to mutual fund investors regardless of the fund’s performance.

As you may expect, these fees amplify losses in years when the fund doesn’t make money. A mutual fund’s creation, distribution, and management are all costly endeavours. Everything costs money, from the portfolio manager’s pay to the quarterly statements for investors.

Those costs are passed on to the shareholders. Because fees vary so much from one fund to the next, failing to pay attention to them might have long-term effects.

The investment or portfolio approach known as “diworsification” is a play on words that implies that too much complexity can lead to poor results. Many mutual fund investors make things too complicated. That is, they buy too many closely related funds and thereby miss out on the risk-reducing benefits of diversification. These investors may have increased the risk in their portfolio. On the other hand, simply owning mutual funds does not imply that you are inherently diversified. A fund that invests just in a specific industry sector or location, for example, is nevertheless relatively hazardous.

To put it another way, too much diversification can result in bad returns. Because mutual funds may contain tiny stakes in a variety of companies, big returns from a few investments may not have a significant impact on the overall return. Dilution can also occur when a successful fund becomes too large. When new money floods into funds with a proven track record, the manager frequently has difficulty identifying acceptable investments to put all of the additional money to good use.

Many investors question whether professional stock pickers are better than you or me. Management is far from perfect, and even if the fund loses money, the management is compensated. Actively managed funds have higher costs, but passive index funds are becoming increasingly popular. Actively managed funds have failed to outperform their benchmark indices throughout multiple time periods, especially after accounting for taxes and fees.

You can request that your mutual fund shares be changed into cash at any time, but unlike stocks that trade all day, many mutual fund redemptions occur only at the conclusion of each trading day.

A capital gains tax is triggered when a fund manager sells a security. When investing in mutual funds, investors who are concerned about the impact of taxes should keep that in mind.

Click here to learn for free from the knowledge base

Who is eligible to take this course?

12th-grade students, undergraduate & post Graduate, Job Seekers, Chartered Accountants, Housewives and Entrepreneurs.

Who is this course for?

- Moreover, the course is designed for new investors who have no prior knowledge of mutual funds or markets. Because the approaches discussed have a long term view, this is appropriate for those in their 20s and those who have just started working (15 to 20 years)

Indeed, this course is for persons who can set away money in mutual funds on a monthly basis. The monthly amount might be as low as Rs. 500.

- Even if you are familiar with mutual funds and investing (perhaps you already do), this course will assist you in selecting the appropriate funds and provide you with numerous investment tips and techniques.

Other courses

Click here for directions