8.1 – Intrinsic Value

The moneyness of an option contract is a classification method wherein each option (strike) gets classified as either – In the money (ITM), At the money (ATM), or Out of the money (OTM) option. This classification helps the trader to decide which strike to trade, given a particular circumstance in the market. However, before we get into the details, I guess it makes sense to look through the concept of intrinsic value again. The intrinsic value of an option is the money the option buyer makes from an options contract provided he has the right to exercise that option on the given day. Intrinsic Value is always a positive value and can never go below 0. Consider this example – Given this, imagine purchasing the 8050CE and having the option to exercise it today rather than waiting for it to expire in 15 days. What I want to know is how much money you would stand to make if you exercised the contract right now. Do you recall that when you exercise a long option, the profit is equal to the option's intrinsic value less the premium paid. Therefore, in order to determine an option's intrinsic value and respond to the question above, we must consult Chapter 3's call option intrinsic value formula. Here is the formula – Intrinsic Value of a Call option = Spot Price – Strike Price Let us plug in the values = 8070 – 8050 = 20

So, if you were to use this option right now, you would be able to earn 20 points (ignoring the premium paid).

Here is a table that determines the intrinsic value for different options strike (these are just arbitrary values I chose to illustrate the point).

I hope this has clarified how the intrinsic value calculation for a specific option strike is done. Here are a few key points I want to highlight:

The amount of money you would earn if you were to exercise the option is its intrinsic value.

An options contract’s intrinsic value is always positive. It could be a positive or negative number.

Call choice Spot price minus strike price is the intrinsic value.

Put choice Strike price minus spot price is intrinsic value.

Before we conclude this conversation, I have the following query for you: Why can’t the intrinsic value be negative, in your opinion?

Let’s use an illustration from the above table to respond to this the spot is 918, the option is 920.

- If you were to exercise this option, what do you get?

- Clearly, we get the intrinsic value.

- How much is the intrinsic value?

- Intrinsic Value = 918 – 920 = -2

- The formula suggests we get ‘– Rs.2’. What does this mean?

- This means Rs.2 is going from our pocket.

- Let us believe this is true for a moment; what will be the total loss?

- 15 + 2 = Rs.17/-

- But we know the maximum loss for a call option buyer is limited to the extent of the premium one pays; in this case, it will be Rs.15/-

- However, if we include a negative intrinsic value, this property of option payoff is not obeyed (Rs.17/- loss as opposed to Rs.15/-). However, to maintain the non-linear property of option payoff, the Intrinsic value can never be negative

- You can apply the same logic to the put option intrinsic value calculation

Hopefully, this should give you some insights into why the intrinsic value of an option can never go negative.

8.2 – Moneyness of a Call option

With our previous discussions on the intrinsic value of an option, the concept of moneyness should be fairly simple to grasp. The moneyness of an option is a classification method that ranks each option strike according to how much money a trader will make if he exercises his option contract today. There are three broad categories –

- In the Money (ITM)

- At the Money (ATM)

- Out of the Money (OTM)

And for all practical purposes, I guess it is best to further classify these as –

- Deep In the money

- In the Money (ITM)

- At the Money (ATM)

- Out of the Money (OTM)

- Deep Out of the Money

The concept of moneyness should be fairly simple to grasp given our previous discussions on the intrinsic value of an option. An option’s moneyness is a classification method that ranks each option strike based on how much money a trader will make if he exercises his option contract today. There are three major categories:

Let us use an example to better understand this. As of today (7th May 2015), the Nifty is trading at 8060. With this in mind, I’ve taken a snapshot of all the available strike prices (the same is highlighted within a blue box). The goal is to categorise each of these strikes as ITM, ATM, or OTM. We’ll talk about the ‘Deep ITM’ and ‘Deep OTM’ later.

The available strike prices trade start at 7100 and go all the way up to 8700, as shown in the image above.

We’ll start with ‘At the Money Option (ATM)’ because it’s the simplest to deal with.

According to the ATM option definition that we posted earlier, an ATM option is the option strike that is closest to the spot price. Given that the spot is at 8060, the closest strike is most likely at 8050. If there was an 8060 strike, 8060 would undoubtedly be the ATM option. However, in the absence of 8060 strikes, the nearest strike becomes ATM. As a result, we classify 8050 as an ATM option.

After we’ve determined the ATM option (8050), we’ll look for ITM and OTM options.

- 7100

- 7500

- 8050

- 8100

- 8300

Do remember the spot price is 8060, keeping this in perspective the intrinsic value for the strikes above would be –

@ 7100

Intrinsic Value = 8060 – 7100

= 960

Non zero value, hence the strike should be In the Money (ITM) option

@7500

Intrinsic Value = 8060 – 7500

= 560

Non zero value, hence the strike should be In the Money (ITM) option

@8050

We know this is the ATM option as 8050 strike is closest to the spot price of 8060. So we will not bother to calculate its intrinsic value.

@ 8100

Intrinsic Value = 8060 – 8100

= – 40

Negative intrinsic value, therefore the intrinsic value is 0. Since the intrinsic value is 0, the strike is Out of the Money (OTM).

@ 8300

Intrinsic Value = 8060 – 8300

= – 240

Because there is a negative intrinsic value, the intrinsic value is 0. Because the intrinsic value is zero, the strike is ineligible (OTM).

You may have picked up on the generalisations (for call options) that exist here, but allow me to reiterate.

OTM are all option strikes that are higher than the ATM strike.

All option strikes that are less than the ATM strike are regarded as ITM.

In fact, I recommend that you take another look at the snapshot we just posted -7100.

NSE displays ITM options on a pale yellow background, while all OTM options have a standard white background. Let’s take a look at two ITM options: 7500 and 8000. The intrinsic values are 560 and 60, respectively (considering the spot is at 8060). The greater the intrinsic value, the more profitable the option. As a result, 7500 strikes are considered “Deep in the Money,” while 8000 strikes are considered “In the Money.”

I would advise you to keep track of the premiums for all of these strike prices (highlighted in the green box). Is there a pattern here? As you move from the ‘Deep ITM’ option to the ‘Deep OTM option,’ the premium decreases. In other words, ITM options are always more expensive than OTM options.

8.3 – Moneyness of a Put option

Let us repeat the exercise to see how strikes are classified as ITM and OTM for Put options. Here’s a look at the various strikes available for a Put option. A blue box surrounds the strike prices on the left. Please keep in mind that at the time of the snapshot (8th May 2015), the Nifty was trading at 8202.

As you can see, there are a wide range of strike prices available, ranging from 7100 to 8700. We will first classify the ATM option before identifying the ITM and OTM options. Because the spot is at 8202, the ATM option should be the closest to the spot. As seen in the above snapshot, there is a strike at 8200, which is currently trading at Rs.131.35/-. This is obviously the ATM option.

We’ll now select a few strikes above and below the ATM to determine ITM and OTM options. Let us consider the following strikes and assess their intrinsic value (also known as moneyness) –

7500

8000

8200

8300

8500

@ 7500

We know the intrinsic value of the put option can be calculated as = Strike – Spot.

Intrinsic Value = 7500 – 8200

= – 700

Negative intrinsic value, therefore the option is OTM

@ 8000

Intrinsic Value = 8000 – 8200

= – 200

Negative intrinsic value, therefore the option is OTM

@8200

8200 is already classified as an ATM option. Hence we will skip this and move ahead.

@ 8300

Intrinsic Value = 8300 – 8200

= +100

Positive intrinsic value, therefore the option is ITM

@ 8500

Intrinsic Value = 8500 – 8200

= +300

Because there is a positive intrinsic value, the option is ITM.

As a result, an easy generalisation for Put options is –

All strikes that are higher than the ATM options are considered ITM.

All strikes with a strike price less than ATM are considered OTM.

And, as the snapshot shows, the premiums for ITM options are significantly higher than the premiums for OTM options.

I hope you now understand how option strikes are classified based on their moneyness. However, you may be wondering why you need to categorise options based on their monetary value. Again, the answer is found in ‘Option Greeks.’ Option Greeks, as you may have guessed, are market forces that act on options strikes and thus affect the premium associated with them.

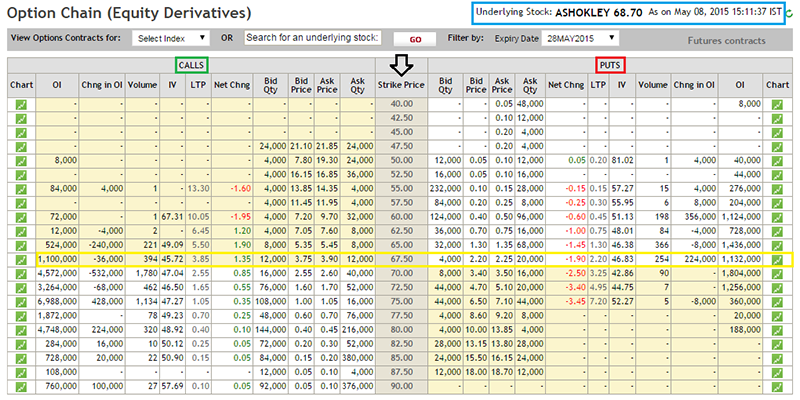

8.4 – The Option Chain

- The underlying spot value is at Rs.68.7/- (highlighted in blue)

- The Call options are on to the left side of the option chain

- The Put options are on to the right side of the option chain

- The strikes are stacked on an increasing order in the centre of the option chain

- Considering the spot at Rs.68.7, the closest strike is 67.5. Hence that would be an ATM option (highlighted in yellow)

- For Call options – all option strikes lower than ATM options are ITM option. Hence they have a pale yellow background

- For Call options – all option strikes higher than ATM options are OTM options. Hence they have a white background

- For Put Options – all option strikes higher than ATM are ITM options. Hence they have a pale yellow background

- For Put Options – all option strikes lower than ATM are OTM options. Hence they have a white background

- The pale yellow and white background from NSE is just a segregation method to bifurcate the ITM and OTM options. The colour scheme is not a standard convention.

Here is the link to check the option chain for Nifty Options.

8.4 – The way forward

After learning the fundamentals of call and put options from both the buyer and seller perspectives, as well as the concepts of ITM, OTM, and ATM, I believe we are all ready to delve deeper into options.

The following chapters will be devoted to comprehending Option Greeks and the impact they have on option premiums. We will devise a method to select the best possible strike to trade for a given market circumstance based on the impact of Option Greeks on premiums. We will also learn how options are priced by running the ‘Black & Scholes Option Pricing Formula’ briefly. The ‘Black & Scholes Option Pricing Formula’ will help us understand why the Nifty 8200 is so volatile.