Options

• Basics of call options

• Basics of options jargon

• How to buy a call option

• How to buy/sell call option

• Buying put option

• Selling put option

• Call & put options

• Greeks & calculator

• Option contract

• The option greeks

• Delta

• Gamma

• Theta

• All volatility

• Vega

21.1 – Background

We have already covered all the significant Option Greeks and their applications in this module. It’s time to comprehend how to use the Black & Scholes (BS) Options pricing calculator to calculate these Greeks. The Black and Scholes options pricing model, from which the name Black & Scholes derives, was first published by Fisher Black and Myron Scholes in 1973. Robert C. Merton, however, developed the model and added a complete mathematical understanding to the pricing formula.

Because of how highly regarded this pricing model is in the financial world, Robert C. Merton and Myron Scholes shared the 1997 Nobel Prize in Economic Sciences. Mathematical concepts like partial differential equations, the normal distribution, stochastic processes, etc. are used in the B&S options pricing model. This module’s goal is not to walk you through the math in the B&S model; instead, you should watch this Khan Academy video.

21.2 – Overview of the model

Consider the BS calculator as a “black box,” which accepts a variety of inputs and produces a variety of outputs. The majority of the market data for the options contract must be provided as inputs, and the outputs are the Option Greeks.

This is how the pricing model’s framework operates:

Spot price, strike price, interest rate, implied volatility, dividend, and the number of days until expiration are the inputs we give the model.

The pricing model generates the necessary mathematical calculation and outputs a number of results.

The output includes all Option Greeks as well as the call and put option’s theoretical price for the chosen strike.

The schematic of a typical options calculator is shown in the following illustration:

The spot price at which the underlying is trading is known as the spot price. Note that we can even substitute the futures price for the spot price. When the underlying of the option contract is a futures contract, we use the futures price. The currency options and the commodity options are frequently based on futures. Utilize the spot price exclusively for equity option contracts.

Interest Rate: This is the market-prevailing, risk-free rate. For this, use the RBI’s 91-day Treasury bill rate. The rate is available on the RBI website’s landing page, which is highlighted in the example below.

Dividend – This is the anticipated dividend per share for the stock, assuming it goes ex-dividend during the expiration period. Assume, for instance, that you want to determine the Option Greeks for the ICICI Bank option contract as of today, September 11th. Consider that ICICI Bank will begin paying a dividend of Rs. 4 on September 18th. Since the September series expires on September 24, 2015, the dividend in this instance would be Rs. 4.

Days remaining before expiration – This is the remaining number of calendar days.

Volatility: You must enter the implied volatility of the option here. You can always extract the implied volatility information by looking at the option chain that NSE provides. Here is an illustration of a snap.

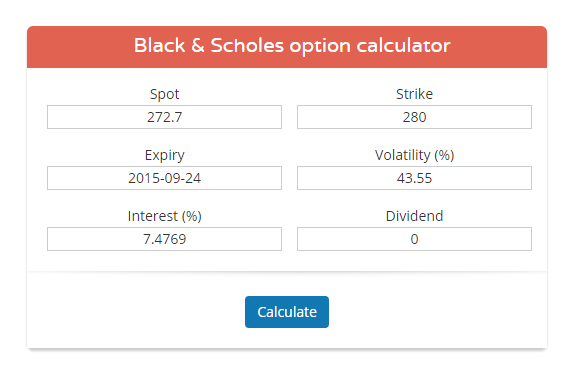

Let’s use this knowledge to determine the ICICI 280 CE option Greeks.

Price at Spot = 272.7

Interest rate equals 7.4769 %

Division = 0

Days until expiration = 1 (today is 23rd September, and expiry is on 24th September)

Volatility is equal to 43.55%

We must enter this data into a typical Black & Scholes Options calculator once we have it. You can calculate the Greeks using the calculator found on our website at https://zerodha.com/tools/black-scholes.

Note the following on the output side:

Calculated is the premium for 280 CE and 280 PE. According to the B&S options calculator, this is the theoretical option price. Ideally, this should coincide with the market’s current option price.

All of the Options Greeks are listed below the premium values.

I’m assuming that by this point you are fairly familiar with the meanings and applications of each Greek word.

One last thing to remember about option calculators: they are primarily used to figure out the Option Greeks and the theoretical option price. Due to differences in input assumptions, minor differences can occasionally occur. It is advantageous to allow for the inescapable modelling errors for this reason. But generally speaking, the

21.3 – Put Call Parity

While we are discussing the topic on Option pricing, it perhaps makes sense to discuss ‘Put Call Parity’ (PCP). PCP is a simple mathematical equation which states –

Put Value + Spot Price = Present value of strike (invested to maturity) + Call Value.

The equation above holds true assuming –

- Both the Put and Call are ATM options

- The options are European

- They both expire at the same time

- The options are held till expiry

For people who are not familiar with the concept of Present value, I would suggest you read through this – http://zerodha.com/varsity/chapter/dcf-primer/ (section 14.3).

Assuming you are familiar with the concept of Present value, we can restate the above equation as –

P + S = Ke(-rt) + C

Where, Ke(-rt) represents the present value of strike, with K being the strike itself. In mathematical terms, strike K is getting discounted continuously at rate of ‘r’ over time‘t’

Also, do realize if you hold the present value of the strike and hold the same to maturity, you will get the value of strike itself,

hence the above can be further restated as –

Put Option + Spot Price = Strike + Call options

Why then should the equality persist? Think about two traders, Trader A and Trader B, to help you better understand this.

A trader holds an ATM. 1 share of the underlying stock and a put option (left hand side of PCP equation)

Trader B is in possession of a call option and cash equal to the strike (right hand side of PCP equation)

Given this situation, both traders should profit equally under the PCP (assuming they hold until expiry). Let’s enter some data to assess the equation:

Underlying = Infosys

Strike = 1200

Spot = 1200

Trader A holds = 1200 PE + 1 share of Infy at 1200

Trader B holds = 1200 CE + Cash equivalent to strike i.e 1200

Assume upon expiry Infosys expires at 1100, what do you think happens?

Trader A’s Put option becomes profitable and he makes Rs.100 however he loses 100 on the stock that he holds, hence his net pay off is 100 + 1100 = 1200.

Trader B’s Call option becomes worthless, hence the option’s value goes to 0, however he has cash equivalent to 1200, hence his account value is 0 + 1200 = 1200.

Let’s take another example, assume Infy hits 1350 upon expiry, lets see what happens to the accounts of both the trader’s.

Trader A = Put goes to zero, stock goes to 1350/-

Trader B = Call value goes to 150 + 1200 in cash = 1350/-

So it is obvious that the equations hold true regardless of where the stock expires, resulting in the same amount of profit for both traders A and B.

All right, but how would you create a trading strategy using the PCP? You’ll have to wait until the next module, which is about “Option Strategies,” to find out, J. There are still two chapters left in this module before we begin the module on option strategies.