Synthetic long & Arbitrage

Basics of stock market

• Induction

• Bull call spread

• Bull put spread

• Call ration Back spread

• Bear call ladder

• Synthetic long & Arbitrage

• Bear put spread

• Bear call spread

• put ration back spread

• Long straddle

• Short straddle

• Max pain & PCR ratio

• Iron condor

6.1 – Background

Imagine being forced to open up long and short positions on Nifty Futures that expire in the same series at the same time. How, and more importantly, why, would you go about doing this?

Both of these issues will be covered in this chapter. Let’s first examine how this can be accomplished, then move on to consider why someone might want to do this (if you are curious, arbitrage is the obvious answer).

Options, as you may already be aware, are extremely flexible derivative instruments that can be used to create any type of payoff structure, including the payoff structure for futures (both long and short futures payoff).

As you can see, the long futures position started at 2360, and since you can’t make money or lose it at that point, it turns the starting point of the position into the breakeven point. If the futures move higher than the breakeven point, you are in the black, and if they move lower than the breakeven point, you are in the red. The amount of profit you make on a move of 10 points upward is exactly equal to the amount of loss you would experience on a move of 10 points downward. The future is also referred to as a linear instrument due to this linearity in the payoff.

The goal of a Synthetic Long is to use options to create a long future payoff that is similar.

4.2 – Strategy Notes

It’s fairly easy to carry out a Synthetic Long; all one needs to do is –

Invest in the ATM Call Option

Vendor Sell ATM Put Option

When you do this, you must ensure that:

The options share the same underlying asset.

has the same expiration

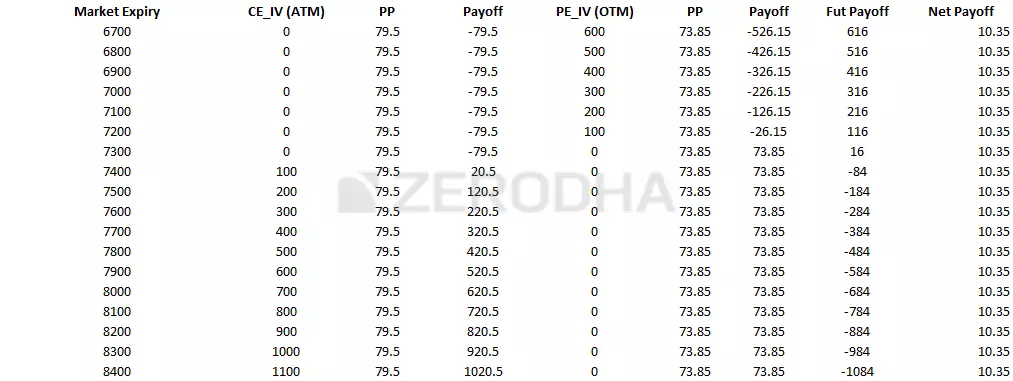

To better understand this, let’s use an illustration. Assuming the Nifty is at 7389, the ATM strike would be 7400. Synthetic Long would require us to short the 7400 PE at 80 and go long on the 7400 CE, which carries a 107-rupee premium.

The difference between the two premiums, or 107 – 80 = 27, would be the net cash outflow.

Consider the following market expiry scenarios:

Situation 1: The market closes at 7200 (below ATM)

At

Intrinsic value of Put Option = Max [Strike-Spot, 0]

= Max [7400 – 7200, 0]

=Max [200, 0]

= 200.

Clearly, since we are short on this option, we would lose money from the premium we have received. The loss would be –

80 – 200 = -120

The total payoff from the Long Call and Short Put position would be –

= -107 – 120

= -227

Scenario 2 – Market expires at 7400 (At ATM)

Both options would expire worthless if the market closes at precisely 7400.

We forfeit the 107 premium that was paid for the 7400 CE option.

We keep the premium for the 7400 PE option, which is 80.

The combined positions’ net payoff would be -27e 80 – 107.

Keep in mind that 27 is also the strategy’s net cash outflow and the difference between the two premiums.

Scenario 3 – Market expires at 7427 (ATM + Difference between the two premiums)

7427 is an interesting level, this is the breakeven point for the strategy, where we neither make money nor lose money.

- 7400 CE – the option is ITM and has an intrinsic value of 27. However, we have paid 107 as premium hence we experience a total loss of 80

- 7400 PE – the option would expire OTM, hence we get to retain the entire premium of 80.

- On one hand, we make 80 and on the other, we lose 80. Hence we neither make nor lose any money, making 7427 the breakeven point for this strategy.

6.3 – The Fish market Arbitrage

Both of the call options, 7600 and 7800, would have zero intrinsic value and would therefore expire worthless.

The premium, which amounts to Rs. 201 for the 7600 CE, is ours to keep; however, we forfeit Rs. 156 for the 7800 CE, leaving us with a net reward of Rs. 45.

Situation 3: The market closes at 7645 (at the lower strike price plus net credit)

If you’re wondering why I chose the level of 7645, it’s because this is where the strategy break even is.

7600 CE’s intrinsic value would be:

Spot – Strike Max [0]

= [7645 – 7600, 0]

= 45

Since we sold this option for 201, the option’s net profit would be

201 – 45

On the other hand, we spent an additional 156 to purchase two 7800 CE. We lose the entire premium because it is obvious that the 7800 CE will expire worthless.

The net payoff is:

156 – 156

= 0

6.3 – The Fish market Arbitrage

I’ll assume you have a fundamental knowledge of arbitrage. Arbitrage is the practice of purchasing assets or goods at a discount and then reselling them at a higher price in order to profit from the price difference. Arbitrage trades are almost risk-free when properly executed. I’ll try to give you a straightforward illustration of an arbitrage opportunity.

Assume you reside near a coastal city where fresh sea fish is in plentiful supply; as a result, the price of fish is very low in your city, let’s say Rs. 100 per kg. The same fresh sea fish is in high demand in the nearby city, which is 125 kilometers away. However, the same fish costs Rs. 150 per kg in this neighboring city.

Given this, if you can buy fish in your city for Rs. 100 and sell it in the neighboring city for Rs. 150, you will undoubtedly pocket the difference in price or Rs. 50. Perhaps you’ll need to factor in logistics and transportation costs and only get to keep Rs. 30 per kilogram instead of Rs. 50. This is still a fantastic deal, and this is a typical fish market arbitrage!

If you can buy fish from your city for Rs. 100 and sell it in the neighboring city for Rs. 150, deducting Rs. 20 for expenses, then Rs. 30 per KG is a guaranteed profit with no risk.

If nothing changes, there are no risks involved. However, if circumstances change, your profitability will as well. Here are some potential changes:

No Fish (opportunity risk) – Let’s say you go to the market one day to buy fish for Rs. 100 but there isn’t any to be found. Then you have no chance of earning Rs. 30.

No Buyers (liquidity risk) – You purchase a fish for Rs. 100 and travel to a nearby town to sell it for Rs. 150 when you discover there are no buyers. You are left with nothing more than a bag of dead fish.

Negative bargaining (risk of execution) The fact that you can “always” bargain to buy at Rs. 100 and sell at Rs. 150 is the basis for the entire arbitrage opportunity. What if you happen to buy at 110 and sell at 140 on a bad day? You must still pay 20 forThe arbitrage opportunity would become less appealing, and you might decide not to do this at all if this continued. transport, this means that instead of the usual 30 Rupee profit you get to make only 10 Rupees.

- No Fish (opportunity risk) – Assume one day you go to the market to buy fish at Rs.100, and you realize there is no fish in the market. Then you have no opportunity to make Rs.30/-.

- No Buyers (liquidity risk) – You buy the fish at Rs.100 and go to the neighboring town to sell the same at Rs.150, but you realize that there are no buyers. You are left holding a bag full of dead fish, literally worthless!

- Bad bargaining (execution risk) – The entire arbitrage opportunity hinges upon the fact that you can ‘always’ bargain to buy at Rs.100 and sell at Rs.150. What if on a bad day you happen to buy at 110 and sell at 140? You still have to pay 20 for transport, this means instead of the regular 30 Rupees profit you get to make only 10 Rupees, and if this continues, then the arbitrage opportunity would become less attractive and you may not want to do this at all.

- Transport becomes expensive (cost of transaction) – This is another crucial factor for the profitability of the arbitrage trade. Imagine if the cost of transportation increases from Rs.20 to Rs.30. Clearly, the arbitrage opportunity starts looking less attractive as the cost of execution goes higher and higher. The cost of the transaction is a critical factor that makes or breaks an arbitrage opportunity

- Competition kicks in (who can drop lower?) – Given that the world is inherently competitive you are likely to attract some competition who would also like to make that risk-free Rs.30. Now imagine this –

- So far you are the only one doing this trade i.e buy fish at Rs.100 and sell at Rs.150

- Your friend notices you are making a risk-free profit, and he now wants to copy you. You can’t really prevent this as this is a free market.

- Both of you buy at Rs.100, transport it at Rs.20, and attempt to sell it in the neighboring town

- A potential buyer walks in and sees there is a new seller, selling the same quality of fish. Who between the two of you is likely to sell the fish to the buyer?

- Clearly given the fish is of the same quality the buyer will buy it from the one selling the fish at a cheaper rate. Assume you want to acquire the client, and therefore drop the price to Rs.145/-

- The next day your friend also drops the price and offers to sell fish at Rs.140 per KG, therefore igniting a price war. In the whole process, the price keeps dropping and the arbitrage opportunity just evaporates.

- How low can the price drop? Obviously, it can drop to Rs.120 (cost of buying fish plus transport). Beyond 120, it does not makes sense to run the business

- Eventually, in a perfectly competitive world, competition kicks in and arbitrage opportunity just ceases to exist. In this case, the cost of fish in neighboring towns would drop to Rs.120 or a price point in that vicinity.

I hope the above discussion gave you a quick overview of arbitrage. In fact, we can define any arbitrage opportunity in terms of a simple mathematical expression, for example with respect to the fish example, here is the mathematical equation –

The cost of purchasing fish in town A minus the price of selling fish in town B equals 20.

We essentially have an arbitrage opportunity if there is an imbalance in the equation above. There are arbitrage opportunities in all kinds of markets, including the fish market, the agricultural market, the currency market, and the stock market, and they are all governed by straightforward mathematical equations.

6.4 – The Options arbitrage

There are arbitrage opportunities in almost every market, but to find them and profit from them, one must be a keen observer of the market. Typically, stock market-based arbitrage opportunities let you carry a profit regardless of the market’s direction while locking in a small but guaranteed profit. Due to this, risk-averse traders tend to favor arbitrage trades quite a bit.

Here, I’d like to talk about a straightforward arbitrage scenario that has its roots in the idea of “Put-Call Parity.” Instead of going over the Put-Call Parity theory, I’ll quickly describe one of its applications.

However, to better understand the Put Call Parity, I highly recommend watching this stunning video from Khan Academy.

Interesting, huh? But you might wonder, what’s the catch?

Fees for transactions!

To determine if it still makes sense to execute this trade, one must take into account the execution costs. Think about this:

Brokerage fees, which are assessed on a percentage basis when using a traditional broker, will take a bite out of your gains. As a result, while you initially make 10 points, you might also end up paying 8 to 10 points in brokerage. Your breakeven point on this trade, however, would be roughly 4-5 points if you were to execute it with a discount broker like Zerodha. You now have even more justification to sign up for a Zerodha account.

STT: Keep in mind that the P&L is realized. as a result, you would have to hold your positions until expiration. If you are long an ITM option, which you will be, you will have to pay a sizable STT at expiration. This will further reduce your profits. Please read on to learn more.

Additional taxes that may apply include service tax, stamp duty, and others.

Therefore, it might not be worthwhile to carry an arbitrage trade for 10 points given these expenses. But it would undoubtedly do so if the reward was higher—say, 15 or 20 points. By squaring off the positions just before expiration with 15 or 20 points, you can even escape the STT trap, though it will take a little time.

For Visit: Click here to know the directions.