Time is money

Remember the proverb “Time is money?” It appears that this adage about time is really significant when it comes to options trading. For the time being, set aside all of the Greek jargon and return to a fundamental understanding of time. Assume you have registered for a competitive exam; you are an innately intelligent candidate with the ability to pass the exam; nevertheless, if you do not give it enough time and brush up on the ideas, you are likely to fail the exam; given this, what is the possibility that you will pass this exam? It all depends on how much time you spend studying for the exam, right? Let us put this in perspective and calculate the likelihood of passing the exam versus the time spent preparing for it.

| Number of days for preparation | Likelihood of passing |

|---|---|

| 30 days | Very high |

| 20 days | High |

| 15 days | Moderate |

| 10 days | Low |

| 5 days | Very low |

| 1 day | Ultra-low |

Obviously, the more days you have to prepare, the more likely you are to pass the exam. Consider the following scenario while adhering to the same logic: If the Nifty Spot is 8500 and you buy a Nifty 8700 Call option, what is the probability that this call option will expire in the money (ITM)? Please allow me to rephrase this query –

- Given that the Nifty is currently at 8500, what is the possibility of the Nifty moving 200 points in the next 30 days, and thus the 8700 CE expiry ITM?

- The possibility of Nifty moving 200 points in the next 30 days is fairly high, hence the likelihood of an option expiring ITM at expiry is quite high.

- What if the time limit is only 15 days?

- Because it is fair to expect the Nifty to move 200 points over the following 15 days, the likelihood of an option expiring ITM at expiry is significant (notice it is not very high, but just high).

- What if the deadline is in 5 days?

- Well, 5 days, 200 points, not sure, therefore the probability of 8700 CE expiring in the money is low.

- What if you only had one day to live?

- The possibility of the Nifty moving 200 points in a single day is fairly low, so I would be reasonably convinced that the option would not expire in the money, so the chance is extremely low.

Is there anything we can deduce from the preceding? Clearly, the longer the period until expiry, the more likely the option will expire in the money (ITM). Keep this in mind when we move our attention to the ‘Option Seller.’ We understand that an option seller sells or writes an option and obtains a premium for it. When he sells an option, he is well aware that he is taking on an unlimited risk with a restricted profit possibility. The prize is only as large as the premium he receives. Only if the option expires worthless does he get to keep his entire payout (premium). Consider the following: – If he is selling an option early in the month, he is well aware of the following:

He is aware of his boundless risk and restricted profit possibilities.

He also understands that the option he is selling has a probability of converting into an ITM option, which means he will not be able to keep his payout (premium received)

In fact, because of ‘time,’ there is always the possibility that the option will expire in the money at any given point (although this chance gets lower and lower as time progresses towards the expiry date). Given this, why would an option seller want to sell options at all? After all, why would you want to sell options when you already know that the option you’re selling has a good chance of expiring in the money? Clearly, time is a risk in the context of option sellers. What if, in order to attract the option seller to sell options, the option buyer promises to compensate for the ‘time risk’ that he (the option seller) assumes?In such a circumstance, it seems reasonable to weigh the time risk versus the remuneration and make a decision, right? This is exactly what happens in real-world options trading. When you pay a premium for options, you are actually paying for –

- Time Risk

- The intrinsic value of options.

In other words, premium equals time value plus intrinsic value. Remember that we defined ‘Intrinsic Value’ earlier in this session as the money you would receive if you exercised your option today. To refresh your recollection, calculate the intrinsic value of the following options assuming the Nifty is at 8423 –

- 8350 CE

- 8450 CE

- 8400 PE

- 8450 PE

We know that the intrinsic value is always positive or zero and can never be less than zero. If the value is negative, the intrinsic value is regarded to be zero. We know that the fundamental value of Call options is “Spot Price – Strike Price” and that of Put options is “Strike Price – Spot Price.” As a result, the intrinsic values for the aforementioned choices are as follows:

- 8350 CE = 8423 – 8350 = +73

- 8450 CE = 8423 – 8450 = -ve value hence 0

- 8400 PE = 8400 – 8423 = -ve value hence 0

- 8450 PE = 8450 – 8423 = + 27

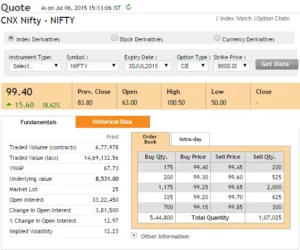

So, now that we know how to calculate an option’s intrinsic value, let us try to partition the premium and extract the time value and intrinsic value. Take a look at the following image –

Details to note are as follows –

- Spot Value = 8531

- Strike = 8600 CE

- Status = OTM

- Premium = 99.4

- Today’s date = 6th July 2015

- Expiry = 30th July 2015

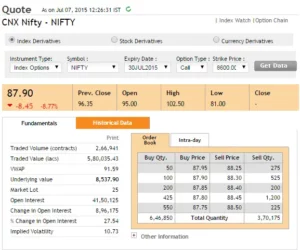

Intrinsic value of a call option – Spot Price – Strike Price, i.e. 8531 – 8600 = 0 (due to the fact that it is a negative number) We already know that Premium = Time value + Intrinsic value. 99.4 + 0 = Time Value This means that the Time value is 99.4! Do you see what I mean? The market is willing to pay Rs.99.4/- for an option with no intrinsic value but plenty of temporal value! Remember that time is money. Here’s a look at the identical contract I signed the next day, July 7th –

The underlying value has increased somewhat (8538), while the option premium has reduced significantly! Let us divide the premium into its intrinsic and time values – Spot Price – Strike Price = 0 (since it is a negative value) We already know that Premium = Time value + Intrinsic value. 87.9 + 0 = Time Value This suggests that the Time value is 87.9! Have you seen the overnight decrease in premium value? We’ll find out why this happened soon. Note: In this example, the premium value decrease is 99.4 minus 87.9 = 11.5. This decrease is due to a decrease in volatility and time. In the following chapter, we shall discuss volatility.For the purpose of argument, assuming both volatility and spot remained constant, the decline in premium would be entirely due to time. This decline is likely to be around Rs.5 or so, rather than Rs.11.5/-. Consider another example:

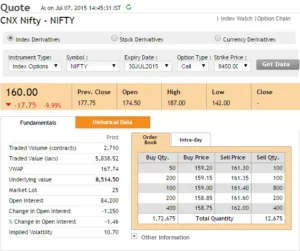

- Spot Value = 8514.5

- Strike = 8450 CE

- Status = ITM

- Premium = 160

- Today’s date = 7th July 2015

- Expiry = 30th July 2015

We know – Premium = Time value + Intrinsic value 8514.5 – 8450 = 64.5 We know – Premium = Time value + Intrinsic value 160 = Time Value + 64.5 This means that the Time value is = 160 – 64.5 = 95.5. As a result, traders pay 64.5 percent of the total premium of Rs.160 for intrinsic value and 95.5 percent for time value. Repeat the computation for all options (calls and puts) and split the premium into time value and intrinsic value.

Movement of time

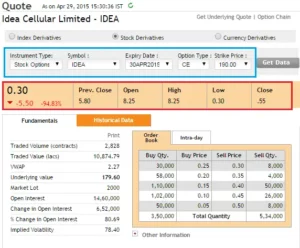

Time, as we know it, travels in just one way. Keep the expiry date as the objective time and consider the passage of time. Obviously, as time passes, the number of days till expiration decreases. Given this, let me ask you this question: If traders are willing to pay as much as Rs.100/- for time value with around 18 trading days to expiry, will they do the same if the time to expiry is only 5 days? Obviously, they would not, would they? With less time to expiry, traders will pay a lower price for time. In reality, here’s a snapshot from the previous months –

- Date = 29th April

- Expiry Date = 30th April

- Time to expiry = 1 day

- Strike = 190

- Spot = 179.6

- Premium = 30 Paisa

- Intrinsic Value = 179.6 – 190 = 0 since it’s a negative value

- Hence time value should be 30 paisa which equals the premium

With only one day till expiry, dealers are willing to pay a time value of 30 paise. However, if the period to expiry was more than 20 days, the time value would most likely be Rs.5 or Rs.8/-. The point I’m trying to make here is that as we approach closer to the expiry date, the time to expiry becomes less and shorter. This means that option buyers will be paying less and less for time value. So, if the option buyer pays Rs.10 as the time value today, he will most likely pay Rs.9.5/- as the time value tomorrow. This brings us to a critical conclusion: “All else being equal, an option is a depreciating asset.”The option’s premium depreciates on a daily basis, which is due to the passage of time.” The next natural issue is how much the premium would reduce on a daily basis due to the passage of time. Theta, the third option in Greek, can assist us answer this question.

Theta

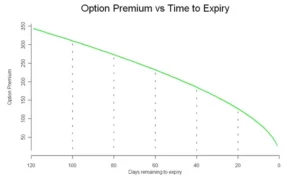

As the expiration date approaches, the value of all options, including calls and puts, decreases. Theta, often known as the time decay factor, is the rate at which an option loses value over time. When all other factors remain constant, theta is stated as points lost per day. Because time moves in only one direction, theta is always a positive number; however, to remind traders that it represents a loss in option value, it is occasionally expressed as a negative number. A Theta of -0.5 suggests that the option premium will decrease by -0.5 points for each passing day. For example, if an option is trading at Rs.2.75/- with a theta of -0.05, it will trade the next day at Rs.2.70/- (provided other things are kept constant).A long option (option buyer) will always have a negative theta, which means that the option buyer will lose money on a daily basis, everything else being equal. Theta for a short option (option seller) will be positive. Theta is a pleasant Greek option seller. Remember that the option seller’s goal is to keep the premium. Given that options lose value on a daily basis, the option seller can benefit by keeping the premium until it loses value due to time. For example, if an option writer sells options at Rs.54 and a theta of 0.75, the identical option will most likely trade at – =0.75 * 3 = 2.25 = 54 – 2.25 = 51.75.As a result, the seller has the opportunity to terminate the position on T+ 3 day by purchasing it again at Rs.51.75/- and gaining Rs.2.25… and this is because of theta! Check out the graph below –

This graph depicts how the premium erodes as the expiry date approaches. This graph is also known as the ‘Time Decay’ graph. From the graph, we can see the following:

- The option loses little value in the beginning of the series, when there are several days till expiry. For example, when the option was 120 days away from expiry, it was trading at 350; yet, when the option was 100 days away from expiry, it was trading at 300. As a result, theta has little effect.

- As the series nears its end, theta has a strong influence. When there were 20 days to expiry, the option was trading around 150, but as we get closer to expiry, the loss in premium appears to increase (option value drops below 50).

So, if you sell options in the beginning of the series, you have the advantage of pocketing a huge premium value (because the time value is quite high), but keep in mind that the premium falls at a low pace. You can sell options closer to expiry for a reduced premium, but the premium decline is significant, which benefits the options seller. Theta is a simple and easy to comprehend Greek letter. We shall return to theta when we consider Greek cross-dependence. But, for the time being, if you understand everything that has been discussed here, you are ready to go. We will now proceed to comprehend the final and most intriguing Greek – Vega!

Conclusion

- Time risk is always paid for by option sellers.

- Intrinsic Value + Time Value Equals Premium

- All else being equal, options lose money every day because to Theta.

- Because time advances in only one direction, Theta is a positive number.

- Theta is a helpful Greek for option sellers.

- When you short naked options at the beginning of the series, you can pocket a significant time value, but the premium drop due to time is minimal.

- When you short an option near to expiry, the premium is low (because to time value), but the premium falls quickly.