Call ratio Back spread

Basics of stock market

• Induction

• Bull call spread

• Bull put spread

• Call ratio Back Spread

• Bear call ladder

• Synthetic long & Arbitrage

• Bear put spread

• Bear call spread

• put ration back spread

• Long straddle

• Short straddle

• Max pain & PCR ratio

• Iron condor

4.1 – Background of call ratio back spread

A fascinating options strategy is the Call Ratio Back Spread. Considering how easy it is to implement and the kind of payoff it offers the trader, I consider this to be interesting. This should undoubtedly be included in your toolbox of tactics. In contrast to bull call spreads and bull put spreads, which are used when one is only mildly bullish on a stock (or index), this strategy is used when one is outright bullish on it.

When using the Call Ratio Back Spread, you will primarily experience the following:

- Unlimited profit if the market goes up

- Limited profit if market goes down

- A predefined loss if the market stay within a range

In simpler words you can get to make money as long as the market moves in either direction.

The Call Ratio Back Spread is typically used for a “net credit,” which means that money starts to arrive in your account as soon as you execute the strategy. In contrast to what you anticipated, the “net credit” is what you earn if the market declines (i.e market going up). On the other hand, if the market does increase, you could stand to gain an endless amount of money. This should also clarify why purchasing a call ratio spread rather than a standard call option is preferable.

So let’s investigate how this operates right away.

4.2 – Strategy Notes

As it involves purchasing two OTM call options and selling one ITM call option, the Call Ratio Back Spread is a three-legged option strategy. This is the standard 2:1 combination. The call ratio back spread must actually be executed in a 2:1 ratio, which means that two options must be purchased for everyone option sold, four must be purchased for every two options sold, and so on.

Let’s use an example where the Nifty Spot is at 7743 and you predict it will reach 8100 by expiration. This is unmistakably a market bullish outlook. In order to use the Call Ratio Back Spread:

Sell one lot of 7600 CE (ITM)

Buy two lots of 7800 CE (OTM)

Make sure –

The Call options belong to the same expiry

Belongs to the same underlying

The ratio is maintained

The trade set up looks like this –

7600 CE, one lot short, the premium received for this is Rs.201/-

7800 CE, two lots long, the premium paid is Rs.78/- per lot, so Rs.156/- for 2 lots

Net Cash flow is = Premium Received – Premium Paid i.e 201 – 156 = 45 (Net Credit)

The call ratio back spread is used in these trades. Let’s examine what would happen to the strategies’ overall cash flow at various levels of expiry.

Please keep in mind that because the strategy payoff is quite flexible, we need to assess it at different levels of expiry.

The market expires in scenario 1 at 7400. (below the lower strike price)

We are aware that a call option’s intrinsic value (upon expiration) is:

Spot – Strike Max [0]

The 7600’s intrinsic worth would be

Max [7400 – 7600, 0]

= 0

Given that we sold this option, we are entitled to keep the premium received, which is Rs. 201.

Since the intrinsic value of the 7800 call option would also be zero, we would forfeit the entire premium, which works out to 78 rupees per lot or 156 rupees for two lots.

Net cash flow would be superior. Paid a premium and received

= 201 – 156

= 45

Scenario 2 – Market expires at 7600 (at the lower strike price)

Both of the call options, 7600 and 7800, would have zero intrinsic value and would therefore expire worthless.

The premium, which amounts to Rs. 201 for the 7600 CE, is ours to keep; however, we forfeit Rs. 156 for the 7800 CE, leaving us with a net reward of Rs. 45.

Situation 3: The market closes at 7645 (at the lower strike price plus net credit)

If you’re wondering why I chose the level of 7645, it’s because this is where the strategy break even is.

7600 CE’s intrinsic value would be:

Spot – Strike Max [0]

= [7645 – 7600, 0]

= 45

Since we sold this option for 201, the option’s net profit would be

201 – 45

On the other hand, we spent an additional 156 to purchase two 7800 CE. We lose the entire premium because it is obvious that the 7800 CE will expire worthless.

The net payoff is:

156 – 156

= 0

Scenario 3 – Market expires at 7700 (half way between the lower and higher strike price)

The 7600 CE would be intrinsically worth 100, while the 7800 would be worthless.

On the 7600 CE, we keep 101 instead of losing 100 from the 201 premium we received, which is 201 – 100 = 101.

The entire Rs. 156 premium on the 7800 CE is lost, so the strategy yields a total payoff of

= 101 – 156

= – 55

Scenario 4 – Market expires at 8100 (higher than the higher strike price, your expected target)

The intrinsic values of the 7600 CE and 7800 CE will be 500 and 300 respectively.

The final result would be:

Premium Paid for 7800 CE – Premium Received for 7600 CE – Intrinsic Value of 7600 CE + (2* Intrinsic Value of 7800 CE)

= 201 – 500 + (2*300) – 156

= 201 – 500 + 600 -156

= 145

Here are some additional levels of expiration and the strategy’s ultimate reward. Keep in mind that as the market rises, so do the profits, but when the market falls, you still make some money, albeit a small amount.

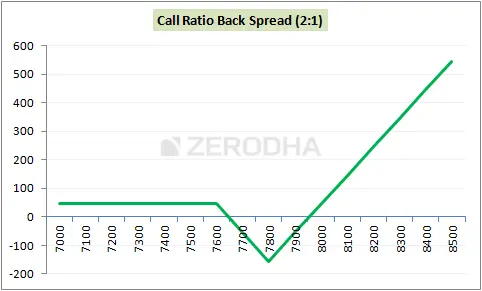

4.3 – Strategy Generalization

Going by the above discussed scenarios we can make few generalizations –

- Spread = Higher Strike – Lower Strike

- Net Credit = Premium Received for lower strike – 2*Premium of higher strike

- Max Loss = Spread – Net Credit

- Max Loss occurs at = Higher Strike

- The payoff when market goes down = Net Credit

- Lower Breakeven = Lower Strike + Net Credit

- Upper Breakeven = Higher Strike + Max Loss

Here is a graph that highlights all these important points –

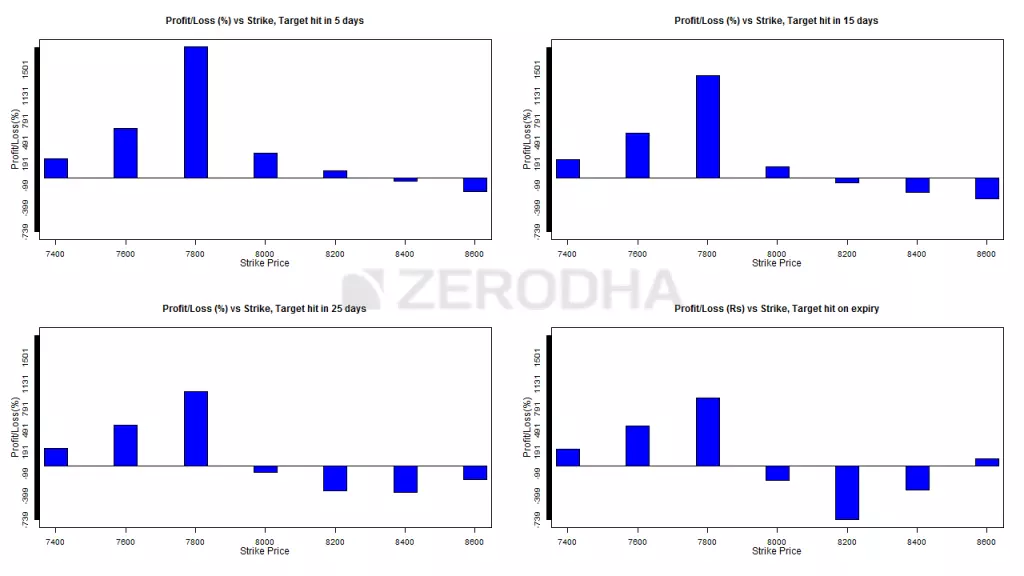

4.4 – Welcome back the Greeks

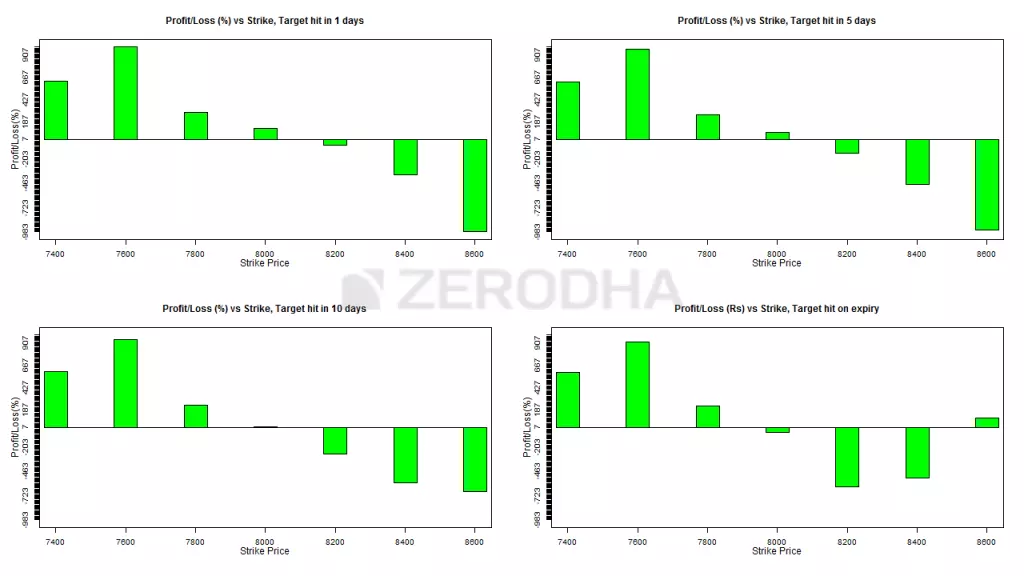

I assume you are already familiar with these graphs. The following graphs demonstrate the profitability of the strategy taking into account the time until expiration; as a result, these graphs assist the trader in choosing the appropriate strikes.

Before understanding the graphs above, note the following –

Nifty spot is assumed to be at 8000

Start of the series is defined as anytime during the first 15 days of the series

End of the series is defined as anytime during the last 15 days of the series

The Call Ratio Back Spread is optimized and the spread is created with 300 points difference

The market is predicted to increase by about 6.25 percent, or from 8000 to 8500. In light of the move and the remaining time, the graphs above indicate that –

Top left on Graph 1 and top right on Graph 2 – The most profitable strategy is a call ratio spread using 7800 CE (ITM) and 8100 CE (OTM), where you would sell 7800 CE and buy 2 8100 CE. This is because you are at the beginning of the expiry series and you anticipate the move over the next 5 days (and 15 days in the case of Graph 2) Do keep in mind that even though you would be correct about the movement’s direction, choosing other far OTM strikes call options usually results in losses.

Graphs 3 and 4 (bottom left and bottom right, respectively) – A Call Ratio Spread using 7800 CE (ITM) and 8100 CE (OTM) is the most profitable option if you are at the beginning of the expiry series and anticipate the move in 25 days (and expiry day in the case of Graph 3). In this scenario, you would sell 7800 CE and buy 2 8100 CE.

You must be wondering why the number of strikes is the same regardless of the time remaining. In fact, this is the key: the call ratio back spread functions best when you sell slightly ITM options and buy slightly OTM options with plenty of time left before expiration. In actuality, all other combinations are in the red, particularly those that include far OTM options.

The best strikes to choose are deep ITM and slightly ITM, i.e., 7600 (lower strike short) and 7900, if you expect the move during the second half of the series and you expect it to happen within a day (or within 5 days, graph 2). (higher strike long). Please take note that this is an ITM and ITM spread rather than the traditional combination of an ITM + OTM spread. In actuality, none of the other combinations work.

Graphs 3 (bottom right) and 4 (bottom left): The best strategy is to use these graphs if you anticipate a move during the second half of the series and that it will occur within 10 days (or on the expiry day, graph 4).Deep ITM and slightly ITM strikes, such as 7600 (lower strike short) and 7900, are the best options (higher strike long). This is in line with what graphs 1 and 2 indicate.

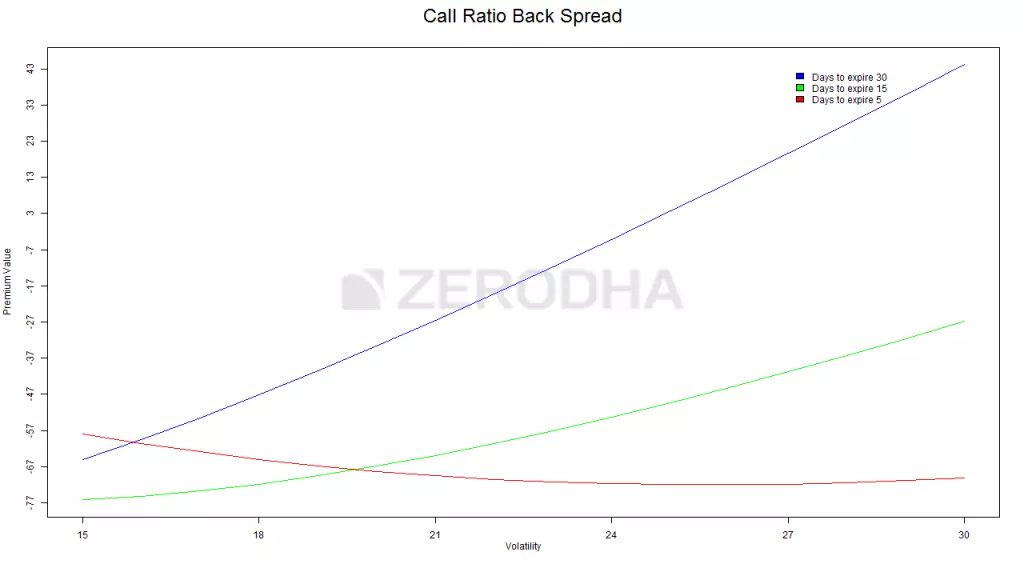

Three colored lines show the relationship between the change in “net premium,” or the strategy payoff, and the change in volatility. These lines give us insight into how an increase in volatility affects the strategy while keeping the time until expiration in perspective.

The blue line indicates that a rise in volatility with plenty of time left before expiration (30 days) is advantageous for the call ratio back spread. As we can see, when volatility rises from 15% to 30%, the strategy’s payoff increases from -67 to +43. This obviously implies that when there is enough time before expiration, in addition to being accurate about the direction of the stock or index, you also need to have a view of volatility. Because of this, even though I believe the stock will rise, I would be a little hesitant to use this strategy at the beginning of the series if volatility is higher than average (say more than double the usual volatility reading)

Green line – This line suggests that, although not as much as in the preceding case, an increase in volatility is advantageous when there are roughly 15 days until expiration. As we can see, when volatility rises from 15% to 30%, the strategy payoff increases from -77 to -47.

Red line: This result is intriguing and illogical. The strategy is negatively impacted by an increase in volatility when there are only a few days left until expiration! Consider that a rise in volatility near the expiration date increases the likelihood that the option will expire in the money, which lowers the premium. So, if you are bullish on a stock or index with a few days left until expiration and you anticipate that volatility will rise during this time, proceed with caution.

For visit: Click here to know the directions.