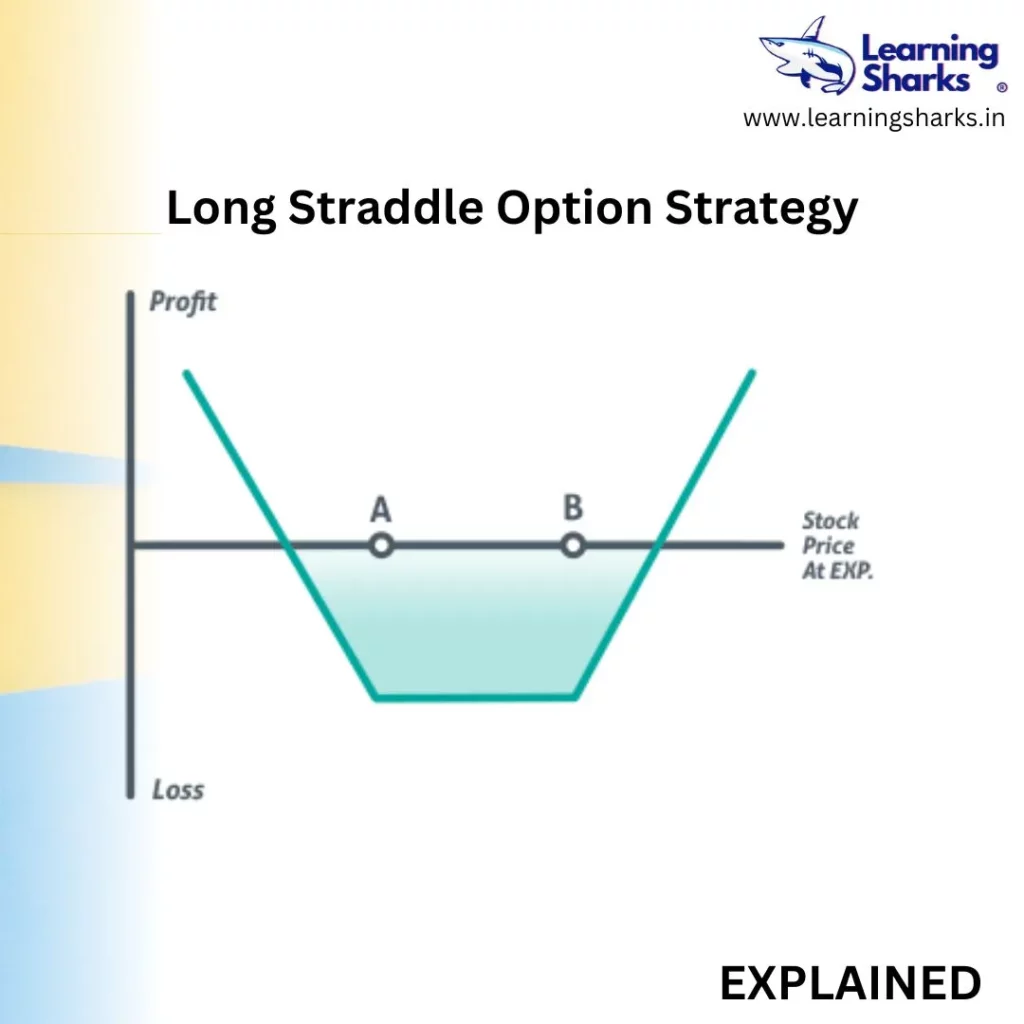

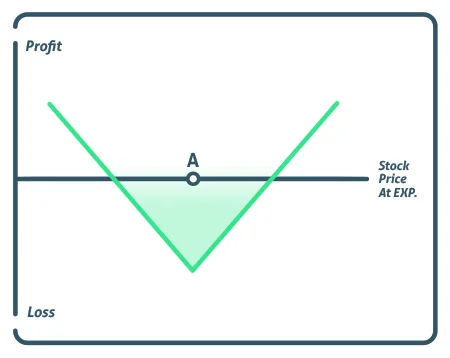

A long straddle is created by purchasing a call option and a put option with the same underlying asset, strike price, and month of expiration. The tactic is employed in cases of extremely erratic market conditions where one anticipates a significant change in the price of a stock, either upward or downward. Such situations can occur when a business makes a significant announcement, reports earnings, or experiences other market-moving events.

As the investor only cares about how far the stock will move and not in which direction, it is a direction-neutral strategy. The trader can make money on the call option if the stock trades higher, but the put option loses value if the stock trades lower. The trader can make money on the put option and let the call expire worthless if the stock trades lower. The potential for profit is limitless, while the risk is only as great as the entry fee. The stock pinning at the strike price at expiration results in the maximum loss.

Profit/Loss

The potential profit from a long straddle strategy is limitless because the position can keep gaining as the stock moves further in either direction.

Maximum Loss = Net Premium Paid

Breakevens

There are two distinct breakeven points in a straddle.

Lower Breakeven = Strike Price of Put – Net Premium

Upper Breakeven = Strike Price of Call + Net Premium

The maximum loss for a trader is the cost of the straddle. Only when a stock pins at the straddles strike price does maximum loss occur.

Maximum Loss = Net Premium Paid

Example

If a stock is trading at Rs100 and one is expecting the stock to either increase or decrease in the near future. An investor can simultaneously purchase Rs100 call, and Rs100 put for the net cost premium of Rs6.

The Rs100 call would be worth Rs25 after deducting the Rs6 premium, making a profit of Rs19 if the stocks traded up to Rs125 at expiration. The Rs100 put option would instead have a value of Rs25, yielding the same Rs19 profit after deducting the premium paid, if the stock dropped in value to Rs75 at expiration.

Conclusion

Since the long straddle consists of two bought options, time decay is an enemy of the tactic. The longer the straddle is on, the more value it loses because the strategy depreciates every day due to time decay.

This tactic typically performs best in erratic markets and has an unlimited potential for profit. The investor will profit from an increase in volatility and need not worry about the direction of the price movement.

Because the premium paid for this strategy is typically high, the amount of the price changes must be significant in order to generate profits.

FOLLOW OUR CHART PATTERNS:https://learningsharks.in/chart-patterns/

FOLLOW OUR PAGE:https://www.instagram.com/learningsharks/?hl=en