Buy one long-term put at a higher strike price and sell one shorter-term put at a lower strike price to create a diagonal spread. The position resembles a long calendar spread with puts in some ways. We want to sell puts with an upside potential, but we also want to protect ourselves in case the stock experience a sharp decline.

The trader can keep selling downside puts in opposition to their long further out put if the execution is correct. As a result, after one short-term put expires, the trader can sell another short-term put that is scheduled to expire the following month, and so on until the long put’s expiration month.

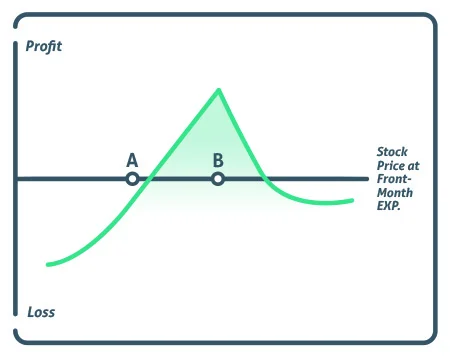

Profit/Loss

The total premiums received from selling short-term downside puts are added together, less the initial premium paid to execute the trade, plus the strike price less the stock price on the last day of the month, to determine the maximum profit.

When the stock rises above the long-term put strike price, the diagonal put spread’s maximum loss is constrained to the cost of the trade.

Breakeven

It is impossible to determine a breakeven point for this dynamic trade because there are so many different scenarios and potential future trades.

Example

A trader could buy the June 100 put for Rs4 and then sell the April 95 put for Rs1.25, resulting in an initial cost of Rs2.75, if XYZ is trading at Rs100 and it is anticipated that it will trade lower over the next four months.

The April put is removed from the account if the stock trades lower than Rs97 by April expiration, and the trader has earned a profit on the long put.

Then, for Rs1.75, they could sell a May 95 strike put. By May expiration, if the stock is trading up to Rs95, the trader will bank Rs1.75 and also have Rs5 of intrinsic value in the long put. Then, for Rs1.25, they could sell a June 90 put. By June expiration, if the stock is trading at Rs92, the June put will also be worthless. In this case, the trader would have opened the trade by paying a premium of Rs2.75 and pocketing premiums of Rs1.75 and Rs1.25 along the way. Additionally, the stock would have an intrinsic value of Rs8. The total profit would be (Rs8+Rs1.75+Rs1.25-Rs2.75), or Rs8.25.

However, if the stock increased to Rs110 after the initial trade, it would be impossible to continue with the strategy because the value of both options would have decreased too much. Both options would expire worthless and the trader would lose his Rs2.75 if the stock never traded lower.

Conclusion

This is a more sophisticated strategy that aims to profit from higher short-term volatility. The stock should decline over time, but slowly, for the best results. That can be challenging, of course, if the strategy’s primary goal is to capture volatility.

FOLLOW OUR CHART PATTERNS:https://learningsharks.in/chart-patterns/

FOLLOW OUR PAGE:https://www.instagram.com/learningsharks/?hl=en