What Is a Blockchain?

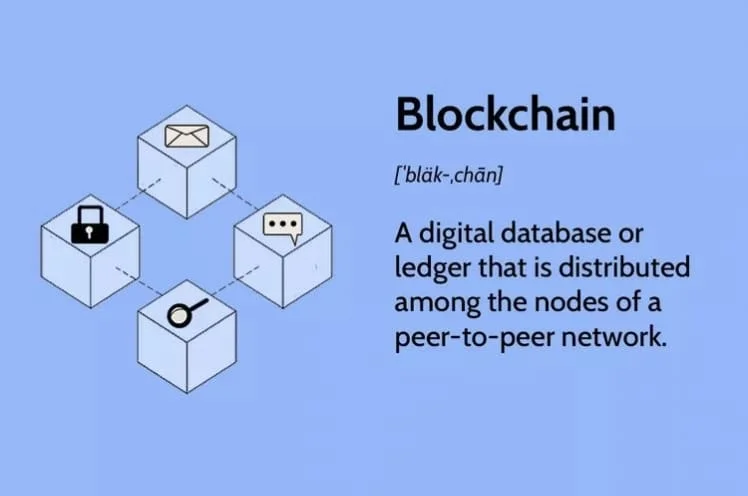

A blockchain is a shared distributed database or ledger between computer network nodes. A blockchain serves as an electronic database for storing data in digital form. The most well-known use of blockchain technology is for preserving a secure and decentralised record of transactions in cryptocurrency systems like Bitcoin.

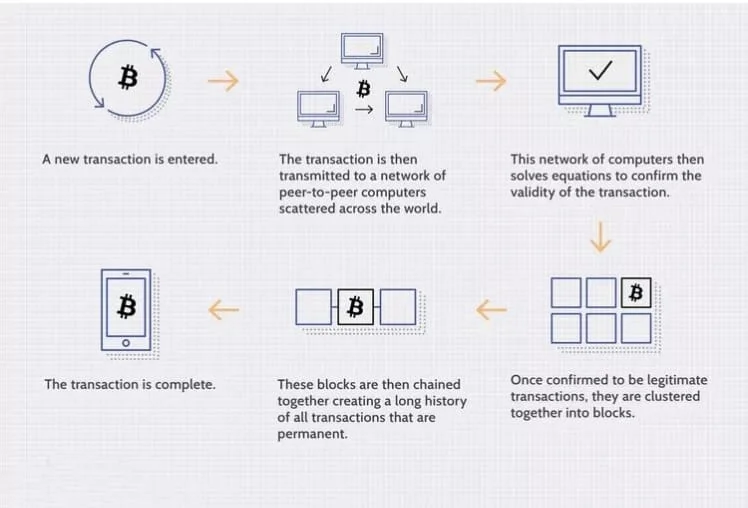

The way the data is organised in a blockchain differs significantly from how it is typically organised. In a blockchain, data is gathered in groups called blocks that each include sets of data. Every additional piece of information that comes after that newly added block is combined into a brand-new block, which is then added to the chain once it is full.

KEY TAKEAWAYS

- A blockchain is a particular kind of shared database that varies from other databases in that it saves data in blocks that are subsequently connected via cryptography.

- A new block is created as each new piece of data arrives. The data is chained together in chronological sequence once the block has been filled with information and is attached to the block before it.

- Blockchain is utilised in the context of Bitcoin in a decentralised manner, ensuring that no one user or group has power but rather that all users collectively maintain control.

How Does a Blockchain Work?

Blockchain aims to make it possible to share and record digital information without editing it. A blockchain serves as the basis for immutable ledgers, or records of transactions that cannot be changed, removed, or destroyed.

The blockchain concept was first put up as a research project in 1991, long before Bitcoin, which was introduced in 2009.

Transaction Process

Attributes of Cryptocurrency

Blockchain Decentralization

Consider a business with a server farm of 10,000 machines that it uses to keep a database with all of its clients’ account information. All of these computers are located in a warehouse that belongs to this corporation, and it has complete authority over each of them as well as the data they hold. But this creates a single point of failure.

This approach aids in creating a clear and precise sequence of events. This prevents any one node in the network from changing the data it contains.

Transparency

Because of the decentralized nature of Bitcoin’s blockchain, all transactions can be transparently viewed by either having a personal node or using blockchain explorers that allow anyone to see transactions occurring live.

As an illustration, exchanges have previously been hacked, and anyone who had Bitcoin stored there lost everything. The stolen Bitcoins are clearly identifiable, despite the hacker’s complete anonymity.

Naturally, the data kept on the Bitcoin blockchain (as well as the majority of others) is encrypted.

Is Blockchain Secure?

Decentralized security and trust are made possible by blockchain technology in a number of ways. To start, new blocks are always chronologically and linearly stored. In other words, they are constantly added to the blockchain’s “end.” It is very difficult to go back and change the contents of a block once it has been added to the blockchain unless a majority of the network has agreed to do so.

When everyone compares their copies to one another, they will notice that this one copy stands out, and the hacker’s version of the chain will be rejected as fraudulent.

The requirement to rewrite every block because their timestamps and hash codes had changed would make such an attack extremely expensive and resource-intensive.

Bitcoin vs. Blockchain

Stuart Haber and W. Scott Stornetta, two researchers interested in implementing a system where document timestamps could not be altered, first proposed the concept of blockchain technology in 1991.

On a blockchain, the Bitcoin protocol is constructed. Bitcoin’s anonymous founder, Satoshi Nakamoto, described the digital currency as “a new electronic cash system that’s fully peer-to-peer, with no trusted third party” in a research paper introducing it.

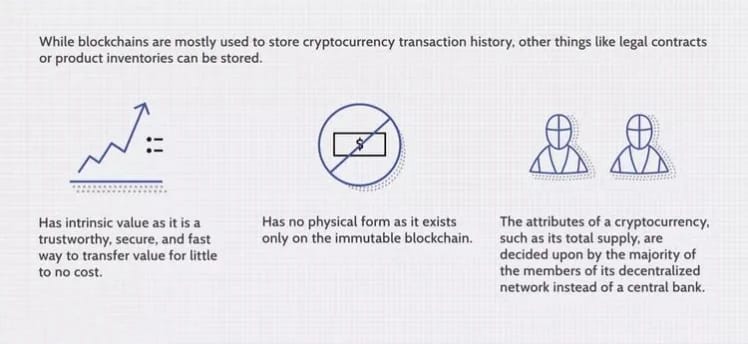

This could take the shape of transactions, votes in elections, goods inventories, state identifications, deeds to properties, and much more, as was previously said.

Blockchain vs. Banks

Blockchain technology has been hailed as a disruptive force for the financial industry, particularly for the payment and banking processes. Banks and decentralised blockchains, however, are very dissimilar.

How Are Blockchains Used?

More than 10,000 additional cryptocurrency systems are currently active on the blockchain. However, it transpires that using a blockchain to store information about other kinds of transactions is also a secure method.

Walmart, Pfizer, AIG, Siemens, Unilever, and numerous more businesses are just a few that have already adopted blockchain technology.

Banking and Finance

Due to the enormous volume of transactions that banks must settle, even if you do make your deposit within business hours, it may still take one to three days for the transaction to be verified. Blockchain, however, is always active.

Given the scale of the amounts involved, even a little period of time during which the money is in transit can be extremely expensive and risky for banks.